As always, let’s start with a recap of my prediction track record:

I may not be “The ETF Whisperer”, but 80% is pretty good! So, what will 2022 hold? First, a few obvious predictions: active ETF launches & inflows will continue accelerating, investors will seek inflation & interest rate-hedged ETFs, ETF innovation will remain focused on solving the income generation challenge, and the industry overall will keep raking-in assets – albeit, a repeat of 2021’s $900+ billion of inflows is unlikely. These all seem obvious to me, but what else will happen this year? Behold, my 2022 ETF predictions…

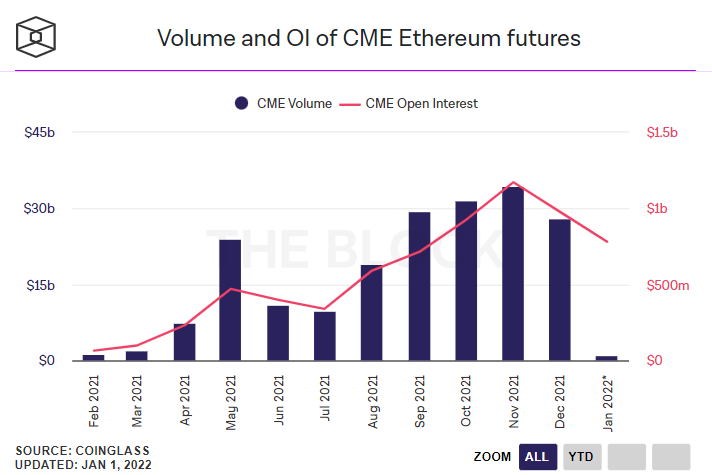

1) First Ethereum Futures ETF is Approved. One of the biggest stories of 2021 was the approval of bitcoin futures ETFs. SEC Chairman Gary Gensler finally got comfortable with a very specific product: CME-traded bitcoin futures held within an ETF structured under the Investment Company Act of 1940. CME futures are regulated by the Commodity Futures Trading Commission (CFTC), which means the federal agency can monitor for things like trading fraud and manipulation. The 1940 Act ETF wrapper offers some additional investor protections that aren’t provided by a 1933 Act product (which would be used to hold “physical” crypto). The combination of a regulated trading venue and (supposedly) more robust structure was enough to get Gensler to the finish line.

Guess what else is CME-traded and can be held in a 40 Act fund? Ethereum futures! If CME-traded bitcoin futures ETFs are good enough for investors, why shouldn’t there be CME-traded ether futures ETFs? While the volume and open interest of CME ether futures is about a third of bitcoin futures, there’s still plenty of liquidity to work with.

Source: The Block

Source: The Block

Source:

Source:

I’ll take this prediction one step further. I think we’ll also see approval of an actively managed crypto futures ETF which holds both bitcoin and ether futures. As for a spot bitcoin ETF… well, I wouldn’t hold my breath. Gensler was crystal clear in his messaging regarding bitcoin futures ETFs. Until we see similar messaging out the SEC regarding a spot product, it’s difficult to envision approval. Gensler simply isn’t comfortable with the lack of regulatory framework around crypto exchanges and the SEC’s ability to surveil these markets. He views crypto as the “Wild West” and won’t be comfortable until he’s the sheriff in town.

2) ESG ETF Closures Spike. This might be the boldest prediction I’ve ever made given that one of the most prevalent 2022 industry predictions is a boom in ESG ETFs. No other segment of the ETF market generates more media hype. I’ll take the other side of that bet. The ESG ETF space is already oversaturated, with too many products and not nearly enough organic investor demand. My prediction is that ESG ETF launches will peak and rollover this year, with an accelerating number of product closures. Why? Many of the same reasons I noted when predicting in 2017 that ESG ETFs would continue garnering more media attention than assets.

The bottom line is that many ESG ETFs don’t look meaningfully different than their non-ESG benchmarks. While costs have continued declining, these products are still more expensive than plain-vanilla ETFs. Even for products that do materially differ from benchmarks, there’s no “one-size fits-all” approach in ESG. In other words, ESG is highly personal. There are significant differences in what people (and ESG ratings agencies) believe constitutes ESG. Just ask 10 people whether they think Tesla is “ESG”.

Source: JUST Capital; Tesla ESG rating

Source: JUST Capital; Tesla ESG rating

Source:

Source:

More importantly, my experience is that many investors are highly skeptical ESG-related funds actually have any meaningful impact on society. I visit with investors of all stripes – young and old, male and female, republican and democrat, you name it. The vast majority believe they can have a much greater impact on society by simply using or not using a company’s products and services. They don’t believe owning or not owning a miniscule portion of a company’s outstanding shares moves the needle.

One other important consideration is direct or custom indexing, which I think could be the death knell for ESG ETFs. Direct indexing offers a much more elegant solution for investors who truly believe they can make a difference through their investments.

ESG ETFs currently represent less than 1.5% of total ETF assets, a large chunk of which comes from institutional investors (pensions, etc) and big issuers using their own products in proprietary model portfolios. I think that 1.5% is already too high. The ESG ETF jig is up.

3) Indie ETF Issuer Boom. 2021 was the beginning of what I believe will be a massive independent ETF issuer boom. Over 40 issuers filed for their first ETF last year, which amounts to just under a quarter of all issuers in the U.S. ETF market since the SPDR S&P 500 ETF (SPY) launched in 1993! The floodgates have opened, primarily the result of 2019’s ETF Rule which streamlined launches and leveled the playing field for new entrants. Add-in the rise of white label ETF issuers such as ETF Architect and Tidal, who are making it significantly easier and cheaper to bring new products to market, and pretty much anyone with a decent idea and some capital can launch an ETF.

Source: ETF.com’s Dan Mika

Source: ETF.com’s Dan Mika

Source:

Source:

I expect to see a significant uptick in Registered Investment Advisory (RIA) firms launching their strategies in an ETF wrapper, along with mutual fund and separately managed account (SMA) conversions to ETFs from smaller asset managers. Investors are demanding the lower cost, more tax-efficient ETF structure. Smaller, independent asset managers can now deliver that structure with much greater ease.

Yes, three ETF firms control 80% of the industry’s market share. Yes, the ETF space is brutally competitive. However, the barriers to entering the ETF Terrordome are lower than ever and issuers such as Roundhill, Simplify, and Cabana have shown the roadmap to success for smaller, boutique firms. It’s absolutely possible to carve out a niche and operate a prosperous ETF company. While the rise of indie ETF issuers began in 2020 and accelerated last year, I believe this will be one of the biggest ETF stories of 2022.

4) ETFs Finally Begin Penetrating 401ks. Retirement plans are the last bastion for mutual funds. Despite their overwhelming success, ETFs have had an extremely difficult time penetrating 401ks. There are several reasons why. Commissioned-based mutual fund brokers still run rampant in the retirement plan space and ETFs don’t pay commissions (therefore, brokers have no incentive to recommend them). There are also additional complexities around ETF trading and record-keeping in 401ks. Lastly, key ETF benefits such as intraday liquidity and tax efficiency simply don’t translate to these plans. So, what changes now?

My prediction is that momentum around mutual fund to ETF conversions is the catalyst that finally tips the scales. This is essentially a combined prediction that the desire (and need) for more fund companies to convert mutual funds will lead to ETFs finally penetrating the 401k space in a meaningful way.

401ks have been a gravy train for mutual fund companies, with a huge chunk of industry assets comfortably collecting fees here. The problem is that 401ks present significant hurdles to completing mutual fund to ETF conversions. Despite the fact that many mutual fund companies are more profitable than ever (thank you bull market!), executives at these companies are seeing the writing on the wall: they absolutely MUST have a well-thought-out ETF strategy moving forward. Mutual fund to ETF conversions are an important part of that strategy and one I believe will spark additional motivation and problem-solving around getting ETFs into 401ks.

The challenge of ETF trading and record-keeping in 401ks has actually been solved. My advisory firm has been offering all-ETF 401k plans for years. Advancements such as fractional shares and commission-free trading have only made this easier and more compelling. While some key ETF benefits don’t translate to retirement plans, that hasn’t stopped millions of investors from owning the products in their personal retirement accounts. Other ETF benefits such as lower costs, additional investment options, and transparency still matter – whether in an IRA or 401k. I’ve seen the fund options in countless 401k plans. I usually want to vomit. While low cost, index-based mutual funds are clearly used in some 401k plans – and are excellent options for investors by the way – there aren’t significant differences compared to index-based ETFs. As an aside, I never understood the argument that 401k plans shouldn’t embrace ETFs because they might encourage participants to trade. 401ks allow participants to buy and sell mutual funds every day. What’s the difference? I digress.

In any event, what has been lacking previously is an incentive for fund companies to push for ETFs in retirement plans. I believe a growing number of companies pursuing mutual fund to ETF conversions will change the dynamics here. If you think ETF growth is impressive now, wait until ETFs invade the last remaining stronghold for mutual funds… which I think begins in earnest this year.

5) Vanguard Share Class Patent Becomes Hot Topic. Vanguard’s ETFs are unique in that they are structured as a share class of their mutual funds. In other words, if you own the Vanguard S&P 500 ETF (VOO), it’s simply a share class of the Vanguard 500 Index mutual fund – it’s the same pool of assets. This structure offers several important advantages, including the ability to better leverage economies of scale, which allows Vanguard to reduce backend costs and charge lower fees to investors. This structure has also helped Vanguard minimize capital gain distributions from its mutual funds since it can wash gains through the ETF share class (this can also work in reverse, to an ETF’s detriment). Here’s the thing: best I can tell, this patent expires in 2023.

The expiration of this patent would theoretically allow ANY fund company to create ETF versions of existing mutual funds, rather than launching clone ETF strategies or pursuing mutual fund to ETF conversions. This solves multiple problems. Instead of hassling with mutual fund to ETF conversions, for example, fund companies can simply create an ETF share class. This allows them to keep milking their cash cow mutual funds and removes the 401k roadblock discussed above. An additional benefit would be the ability to reduce some nasty mutual fund capital gain distributions.

My prediction is the Vanguard patent becomes THE hot topic of discussion in the latter half of the year. The ability for fund companies to offer ETFs as a share class of existing mutual funds could impact everything from Vanguard’s ETF dominance to ETF taxation (which became a talking point last year) to the pace of mutual fund conversions.

One note: the 2019 ETF Rule doesn’t apply to share class ETFs as there are some concerns around whether this structure is in the best interests of investors (i.e. could the activities within the mutual fund share class negatively impact the ETF share class?). This could cause smaller issuers to look away from this structure due to additional costs and headaches. But, again, that would only spark additional conversation around including this structure as part of the ETF Rule.